A portal website bringing together vital information about natural gas and natural gas vehicles.

Vermont Policy Data

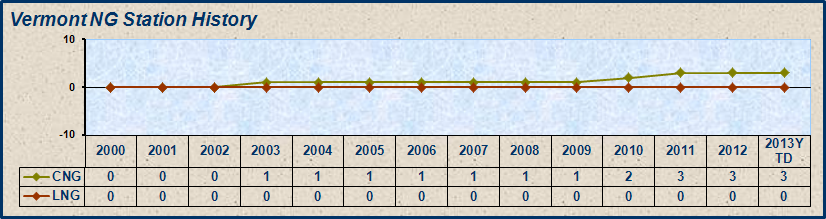

Summary

Vermont offers several incentive programs through their Clean Energy Development Fund. The State also offers a tax credit for AFV research and development firms engaged in that business in Vermont.

Vermont has more legislation that concerns or includes natural gas than any other type of alternative fuel. Vermont has rules for AFV acquision for within state agencies, and AFV promotion was assigned to the Vermont Climate Cabinet in 2011, and the state has a robust Energy Plan that includes transportation requirements that include AFVs.

Vermont also currently imposes an additional tax of 2% of the average quarterly retail price as a Motor Fuel Transportation Infrastructure Assessment (Gasoline) as of this writing was .0645 ¢ / Gallon. This value changes quarterly, so click the Reference to learn the current quarterly rate.

** Includes a 1.0 ¢ / Gallon Petroleum Clean Up fee.

*** Includes a 3.0 ¢ / Gallon Petroleum Clean Up fee.

IFTA - IFTA taxes are applied to vehicles of 3+ axles, or weighing more than 26,000 pounds. IFTA tax tables can be found here.

Incentives

Alternative Fuel and Advanced Vehicle Research and Development Tax Credit

Vermont businesses that qualify as a high-tech business involved exclusively in the design, development, and manufacture of alternative fuel vehicles, hybrid electric vehicles, all-electric vehicles, or energy technology involving fuel sources other than fossil fuels are eligible for up to three of the following tax credits: 1) payroll income tax credit; 2) qualified research and development income tax credit; 3) export tax credit; 4) small business investment tax credit; and 5) high-tech growth tax credit. Certain limits and restrictions apply. (Reference Vermont Statutes Title 32, Chapter 151, Section 5930a, c, f, g, and k)

Alternative Fuel Vehicle (AFV) Acquisition Requirements

The Vermont Department of Buildings and General Services must consider AFVs when purchasing vehicles for state use, provided that the alternative fuel is suitable for the vehicle's operation, is available in the region where the vehicle will be used, and is competitively priced with conventional fuels. (Reference Vermont Statutes Title 29, Chapter 49, Section 903)

State Agency Energy Plan Transportation Requirements

The Vermont Agency of Administration developed and oversees the implementation of the State Agency Energy Plan (Plan). The Agency of Administration must modify the Plan as necessary and re-adopt it on or before January 15 of each fifth year. As specified in the 2010 Plan, the Vermont Agency of Transportation must continue to use 5% biodiesel (B5) in its fleet of heavy-duty vehicles. The Vermont Department of Buildings and General Services must continue to use hybrid electric vehicles and Partial Zero Emission Vehicles in its fleet, while adjusting purchases based on annual fleet selection monitoring and available vehicle technology. All state agencies must investigate the use of additional alternative fuel and advanced technology vehicles, as well as the necessary fueling infrastructure, such as incorporating electric vehicle supply equipment at appropriate state facilities. The Plan specifies the responsibilities of the Climate Neutral Working Group (Working Group). All state government agencies, offices, and departments must purchase the most fuel-efficient vehicles available in each vehicle class according to specifications set by the Working Group. The Working Group must consider vehicles that meet high fuel economy standards and emit reduced levels of greenhouse gases, criteria pollutants, and hazardous air contaminants. Additionally, the Working Group must expand education and tracking related to anti-idling campaigns for state fleet vehicles and private sector vehicles operating on state owned property, and conduct a survey to determine the level of government employee participating in carpooling, vanpooling, and other commuting options. (Reference Vermont Statutes Title 3, Chapter 45, Section 2291, and Executive Order 14-03, 2003)

Tax bill that among other things includes a study to evaluate impact of imposing the gross receipts tax on CNG and LNG. NGVAmerica records indicate that natural gas is subject to 6% sales tax but not the state motor fuel excise tax. Reference - HB873 Bill History, Reference - HB873 Bill Text Status: passed House 3/24/16; Conference Report adopted by House and Senate 5/6/13 but the provisions related to natural gas study were struck; enacted 5/25/16.

2015 Session - Proposed Legislation

HB-488

Transportation infrastructure bill. Proposes new motor fuel tax as follows: 12.1 cent, plus 3.96 cent or 2% of wholesale price (whichever is greater), plus the greater of 13.4 cent, or 4% of the tax adjusted wholesale price or 18 cents (whichever is less). Reference - HB488 Bill History, Reference - HB488 Bill Text

Imposes carbon tax on motor fuels and over time phases out and repeals the sales tax on fuels. The carbon tax rates cover gasoline, diesel, natural gas and other fuels but electricity appears uncovered. The rates are initially phased in and the sales tax reduced to 3% and then 1% and then 0. When fully implemented - July 1, 2019 - the rates per gallon are as follows: gasoline $0.89, diesel $1.01, natural gas $0.55 (per Therm). Effective date is July 1, 2013. Reference - HB506 Bill History, Reference - HB506 Bill TextPending: House Ways and Means Committee

HB-510

Long bill. Includes study of impact of electric, natural gas and propane vehicles on state revenues. Starting July 1, 2013 a 6% sales tax will apply to sales of natural gas. However, propane is not addressed. The bill calls for a written report to be submitted by December 15, 2013. Reference - HB510 Bill History, Reference - HB510 Bill TextSigned by Governor 4/29/2013; Act No. 12.

This state was last examined and updated in July, 2016.