A portal website bringing together vital information about natural gas and natural gas vehicles.

Michigan Policy Data

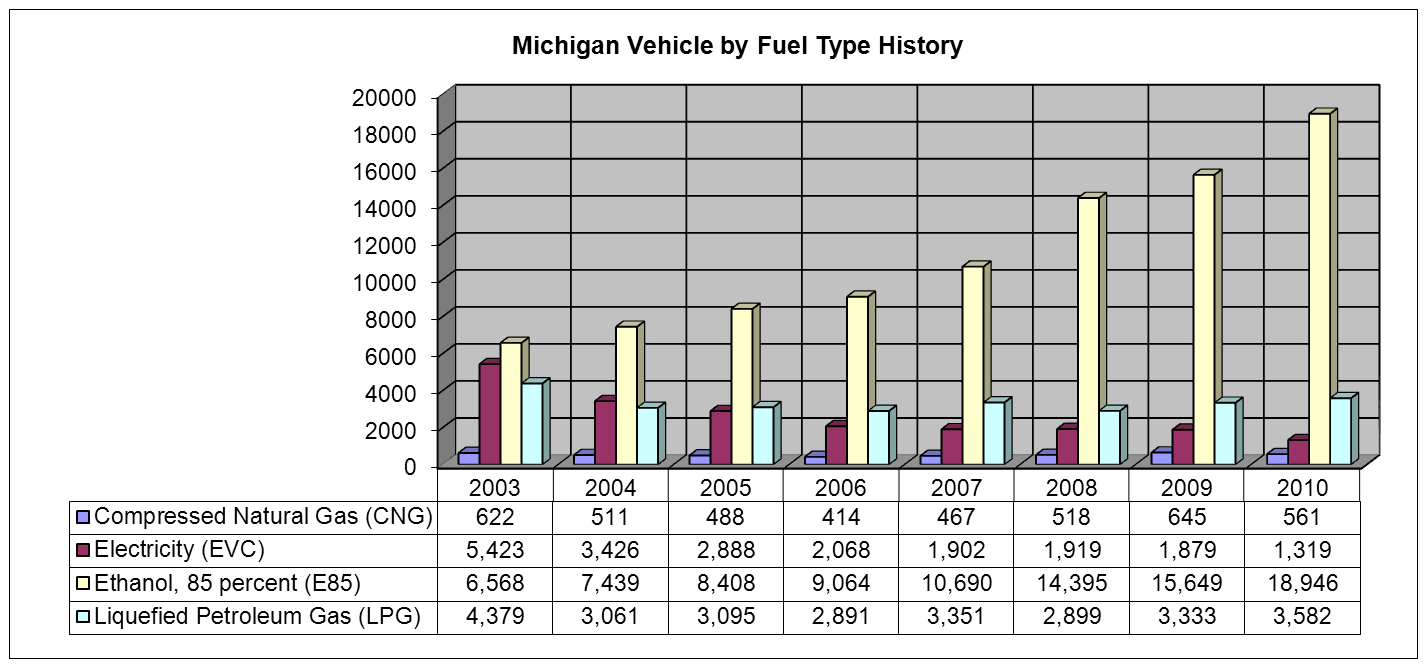

Summary

Michigan currently has multiple incentives available for AFV infrastructure development and vehicle research. Further, AFVs are exempt from Michigan's vehicle inspection requriements, and through December, 2012, qualifying AFVs are exempt from property taxes.

IFTA - IFTA taxes are applied to vehicles of 3+ axles, or weighing more than 26,000 pounds. IFTA tax tables can be found here.

Incentives

Alternative Fuel Development Property Tax Exemption

A tax exemption may apply to industrial property that is used for, among other purposes, high-technology activities or the creation or synthesis of biodiesel fuel. High-technology activities include those related to advanced vehicle technologies such as electric, hybrid electric, or alternative fuel vehicles and their components. To qualify for the tax exemption, an industrial facility must obtain an exemption certificate for the property from the Michigan State Tax Commission. (Reference Michigan Compiled Laws 207.552 and 207.803)

Alternative Fuel Vehicle (AFV) Emissions Inspection Exemption

Dedicated AFVs powered by compressed natural gas, propane, electricity, or any other source as defined by the Michigan Department of Transportation are exempt from emissions inspection requirements. (Reference Michigan Compiled Laws 324.6311 and 324.6512)

Natural Gas Fueling Station Air Quality Permit Exemption

The Michigan Department of Environmental Quality requirement to obtain an installation permit does not apply to qualified natural gas storage and handling equipment at dispensing facilities. (Reference Michigan Air Pollution Control Rule 336.1284

Laws & Regs

Alternative Fuel Excise Tax

Beginning January 1, 2017, alternative fuels will be taxed equal to the motor fuel tax on a gallon equivalent basis. Alternative fuels include natural gas, propane, hydrogen, and hythane. A gallon equivalent is defined as 5.660 pounds (lbs.) of compressed natural gas, 6.06 lbs. of liquefied natural gas, 480.11 standard cubic feet of hydrogen, and 162.44 standard cubic feet of hydrogen compressed natural gas. A gallon of propane is measured as 4 quarts or 3.785 liters. (Reference Michigan Compiled Laws 207.1151 and 207.1152

Alternative Fuel Dealer and Commercial User License

Beginning January 1, 2017, alternative fuel dealers and alternative fuel commercial users must apply for a license from the Michigan Department of Treasury. Commercial users are defined as those operating vehicles with three or more axles, or two axles and a gross vehicle weight rating exceeding 26,000 pounds, that operate in more than one state. Alternative fuel dealers must pay a license fee of $500 and commercial users must pay a license fee of $50. For the purpose of this requirement alternative fuels include natural gas, propane, hydrogen, and hythane. (Reference Michigan Compiled Laws 207.1151 and 207.211)

Alternative Fuel Commercial User Tax

Beginning January 1, 2017, an alternative fuel commercial user that has not paid fuel taxes to an alternative fuel dealer must file a monthly report with the Michigan Department of Treasury (Department) to determine taxes owed under Michigan Compiled Laws 207.1152. By the twentieth day of each month, users must file the report detailing the number of gallons or gallon equivalents of alternative fuel consumed during the preceding month. Alternative fuel commercial users must pay the full amount of tax due to the Department at the time of filing the report. (Reference House Bill 5572, 2016, and Michigan Compiled Laws 207.1154

Proposed Bills

[printfriendly]

2015 Proposed NGV Legislation

HB-5572

Starting Jan. 1, 2017 authorizes a commercial user of CNG who fuels at a station or stations owned or leased by that commercial user and that are not open or available to the public, to pay the excise tax rate specified in section 152 on a diesel gallon equivalent basis. A DGE is set out as 6.38 lb. or 142.78 cubic feet of CNG. This would effectively equalize the tax rate for some commercial users so that CNG and LNG are taxed on a DGE basis. Legislation enacted last year imposes the LNG tax on a DGE of 6.06 pounds. Reference - HB5572 Bill History, Reference - HB5572 Bill Text Status: passed House 9/21/16; passed Senate 10/20/16; signed by governor 11/2/16

Amends motor fuel gasoline tax so that CNG pays on GGE basis (5.66 lbs. or 126.67 cu. ft.) and LNG pays diesel rate based on DGE of 6.06 lbs. Replaces current base tax of 19 cent on gasoline and 15 cent on diesel with a tax that is based on 7.5 percent of the wholesale price of these fuels to take effect April 1, 2015, and that is increased each year afterwards by 1% until maxing out at 13.5% in 2021. Note the bill enacted last year includes tax of 14.9 percent. Requires retailers to advertise price of fuel in gallon equivalent units. Reference - HB4317 Bill History, Reference - HB4317 Bill Text

HB-4337

This bill focuses exclusively on alternative fuel and incorporates the current DGE and GGE definitions for CNG and LNG as already enacted under Michigan law. However, it appears to clarify that unlike the other bills under consideration, that the excise tax for alternative fuels is tied to the gasoline tax and not the higher diesel or motor fuel tax. This needs to be confirmed. Reference - HB4337 Bill History, Reference - HB4337 Bill Text

HB-4612

Increases registration fee by $30 for hybrid electric vehicles and by $100 for a battery electric vehicle. Also requires manufacturer to report annually to the state on any hybrid or electric vehicles that are offered for sale in the state. Reference - HB4612 Bill History, Reference - HB4612 Bill Text

HB-4614

Motor fuel tax. Imposes diesel rate on LNG per diesel gallon equivalent; diesel tax is 6% of wholesale price. CNG would pay the gasoline rate (6% gasoline wholesale price) but not sure what unit would be used; the only term used in the bills is DGE. This bill references sections of code enacted in January but not yet effective. Also indicates that it only takes effect if other bills are enacted (see HB 4615, 4616). Reference - HB4614 Bill History, Reference - HB4614 Bill Text Status: June 10 Reprint - references "gallon equivalent" and no longer singles out DGE. Also ties the 6% tax rate for alternative fuels to the price of those alternative fuels and not gasoline or diesel (unless average alternative fuel prices are not available). Effective date is Oct. 1, 2017. Signed by Governor 11/9/15

HB-4615

Motor fuel tax. Starting Oct. 1, 2015 would raise the diesel tax from 15 to 19 cent (gasoline already pays 19 cent). The state also imposes additional tax of 6% sales tax on gasoline and diesel. Provides that CNG, LNG, and most other alternative fuels are to be taxed like diesel fuel and based. CNG and LNG would pay per DGE using 6.380 lbs. or 6.06 lbs. as a DGE, respectively. The new tax on CNG and LNG would apply Oct. 1, 2015 for retailers, Jan. 1, 2016 for commercial users, and July 1, 2016 for all other users. The fuel tax would be adjusted each year for inflation or by 5% whichever is less but would not be lower than the rate in effect on Oct. 1, 2015. Residential users appear to be covered by the new tax but would have until July 1, 2016 to start complying; payments would be quarterly instead of monthly for non-commercial users. Reference - HB4615 Bill History, Reference - HB4615 Bill Text 6/10/15 subst. version replaces CNG DGE with GGE of 5.66 lb. or 126.67 cu. ft. for tax.

HB-4616

Motor fuel tax changes. This bill incorporates changes to the taxation of motor carriers. Reference - HB4616 Bill History, Reference - HB4616 Bill Text Status: Substitute passed Senate 7/1/15; to House for concurrence; passed S 7/1/15; both House and Senate concur to all changes. Signed by Governor 11/10/15

HB-4736

Imposes new vehicle registration fees including increased rates on electric and hybrid electric vehicles. The fee for hybrid vehicles is additional $30 for vehicles less than 8,001 lbs. and $100 for larger vehicles. For non-hybrid electric vehicles the additional fee is $100 for vehicles less than 8,001 and $200 for larger vehicles. Effective Jan. 1, 2107. Rates increase if gasoline tax increases. Reference - HB4736 Bill History, Reference - HB4736 Bill Text Status: 10/21/15 passed House; Senate amended 11/3/15; House concurs 11/3/15. Signed by Governor 11/10/15

HB-4738

Increases tax on motor fuels. Equalizes the diesel tax so that it pays the 19 cent imposed on gasoline; this would take effect Oct. 1, 2017. The rates would increase to 22.3 cents starting on Oct. 1, 2018. The rates will then be adjusted each year based on inflation factor. Beginning Jan. 1, 2018, commercial user of natural gas shall pay the motor fuel tax per GGE 5.66 lbs. or 126.67 cu. ft. for CNG and 6.06 lbs. for LNG. Update: enacted version imposes new tax of 26.3 cents on gasoline and diesel fuel and other motor fuels starting Jan. 1, 2017. The alternative fuel tax goes into effect later (Jan. 1, 2018 for non-commercial users who otherwise are not purchasing retail fuel). Reference - HB4738 Bill History, Reference - HB4738 Bill Text Status: Passed House 10/21/15; passed Senate 11/3/15 w/ amendments; House concurs 11/3/15. Signed by Governor 11/10/15

SB-341

Amends motor fuel tax so that CNG pays gasoline base rate per GGE and LNG pays diesel base rate per DGE. Also includes CNG GGE of 5.66 lbs. or 126.67 cu. ft., and LNG DGE of 6.06 lbs. Increases fee charged for retailers from $50 to $500, and charges commercial users a fee of $50. Retailers and commercial users would have to fie taxes monthly, while other users would have to file quarterly. The requirements would go into effect for commercial users starting July 1, 2016 and for other users like residential users, would take effect Jan. 1, 2017. Reference - SB341 Bill History, Reference - SB341 Bill Text